Over the past six months, Central Garden & Pet’s stock price fell to $36.13. Shareholders have lost 5.7% of their capital, which is disappointing considering the S&P 500 has climbed by 1%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Central Garden & Pet, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why you should be careful with CENT and a stock we'd rather own.

Why Do We Think Central Garden & Pet Will Underperform?

Enhancing the lives of both pets and homeowners, Central Garden & Pet (NASDAQ:CENT) is a leading producer and distributor of essential products for pet care, lawn and garden maintenance, and pest control.

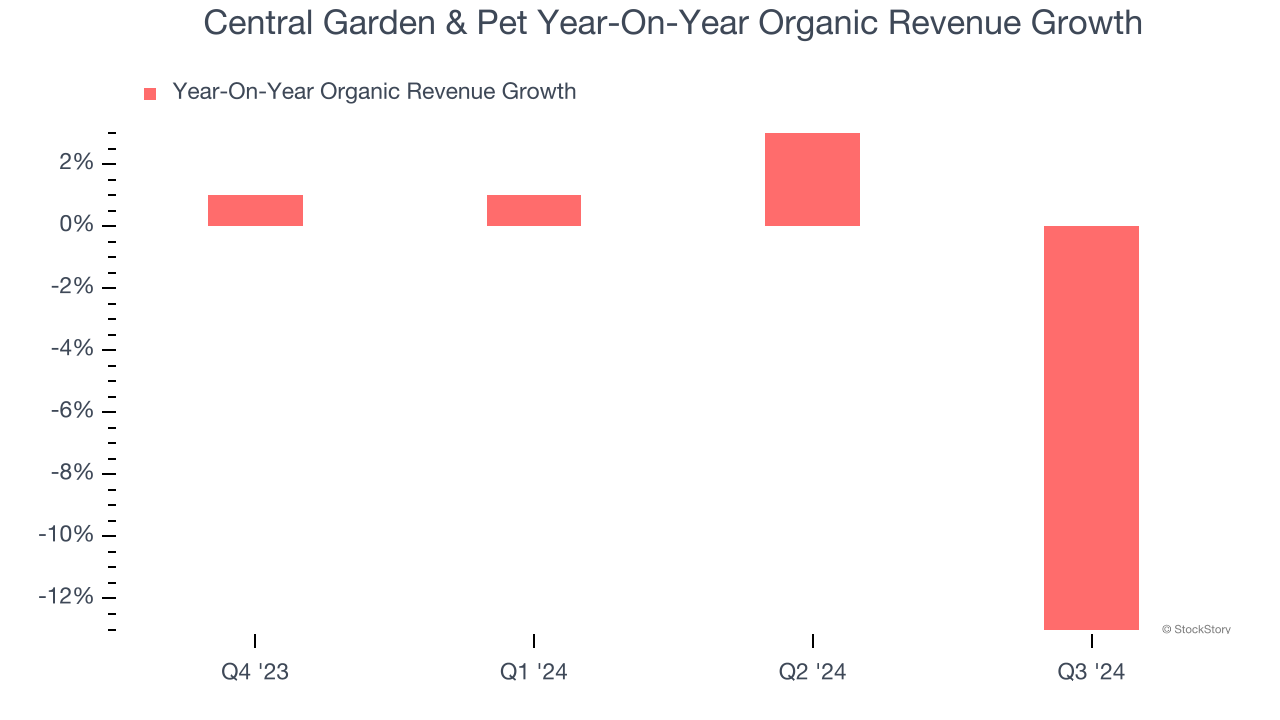

1. Core Business Falling Behind as Demand Declines

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Central Garden & Pet’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 2% year on year.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Central Garden & Pet’s revenue to stall. While this projection indicates its newer products will fuel better top-line performance, it is still below the sector average.

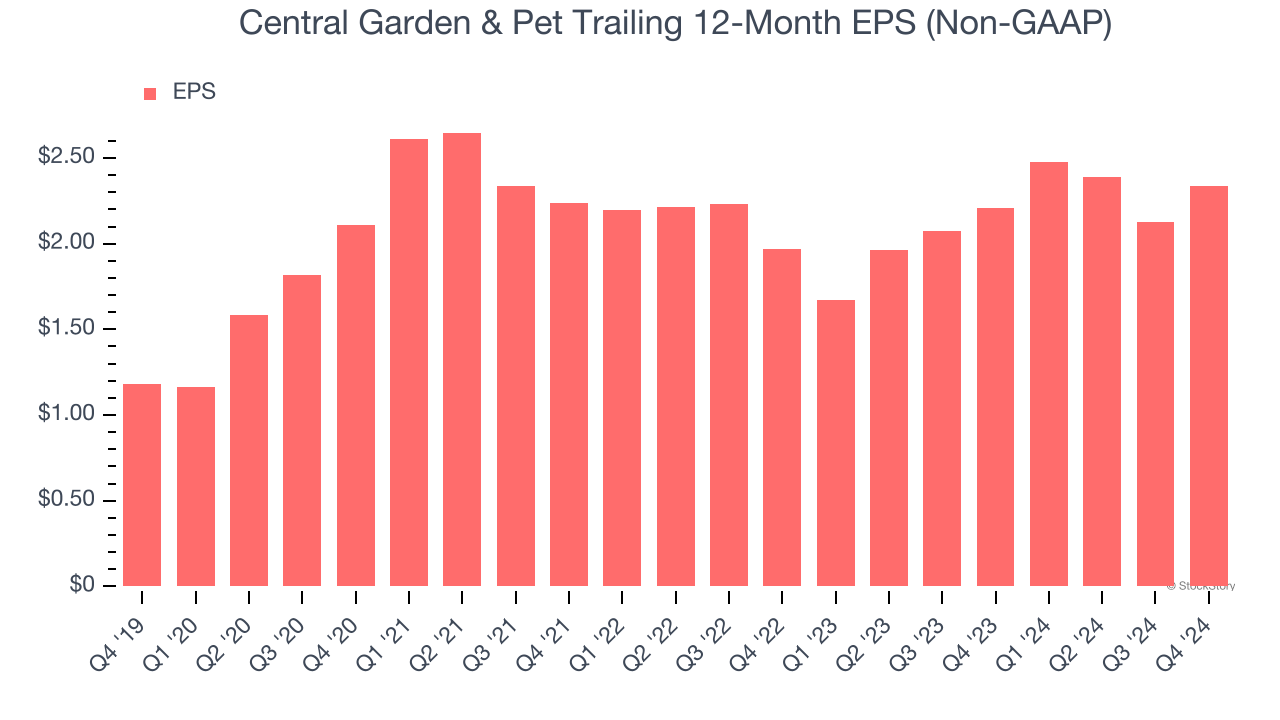

3. EPS Barely Growing

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Central Garden & Pet’s EPS grew at an unimpressive 1.5% compounded annual growth rate over the last three years. On the bright side, this performance was better than its 1.5% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

Final Judgment

Central Garden & Pet falls short of our quality standards. After the recent drawdown, the stock trades at 16.7× forward price-to-earnings (or $36.13 per share). This multiple tells us a lot of good news is priced in - we think there are better investment opportunities out there. We’d suggest looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Central Garden & Pet

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.